Weekly Roundup 2022-11-18 – Walmart and Amazon

Lunar Capital Weekly Roundup

| Index / Fund / Rate | Start of Year | Last week | This Week | % change YTD |

|---|---|---|---|---|

| JSE ALSI | 73 723 | 72 115 | 72 577 | -1,55% |

| NASDAQ Composite | 15 833 | 11 323 | 11 146 | -29,60% |

| S&P 500 | 4 797 | 3 993 | 3 965 | -17,34% |

| Prime Lending Rate | 7,25% | 9,75% | 9,75% | 34,48% |

| Lunar BCI WW Flexible Fund | 165,68 | 146,33 | 147,16 | -11,18% |

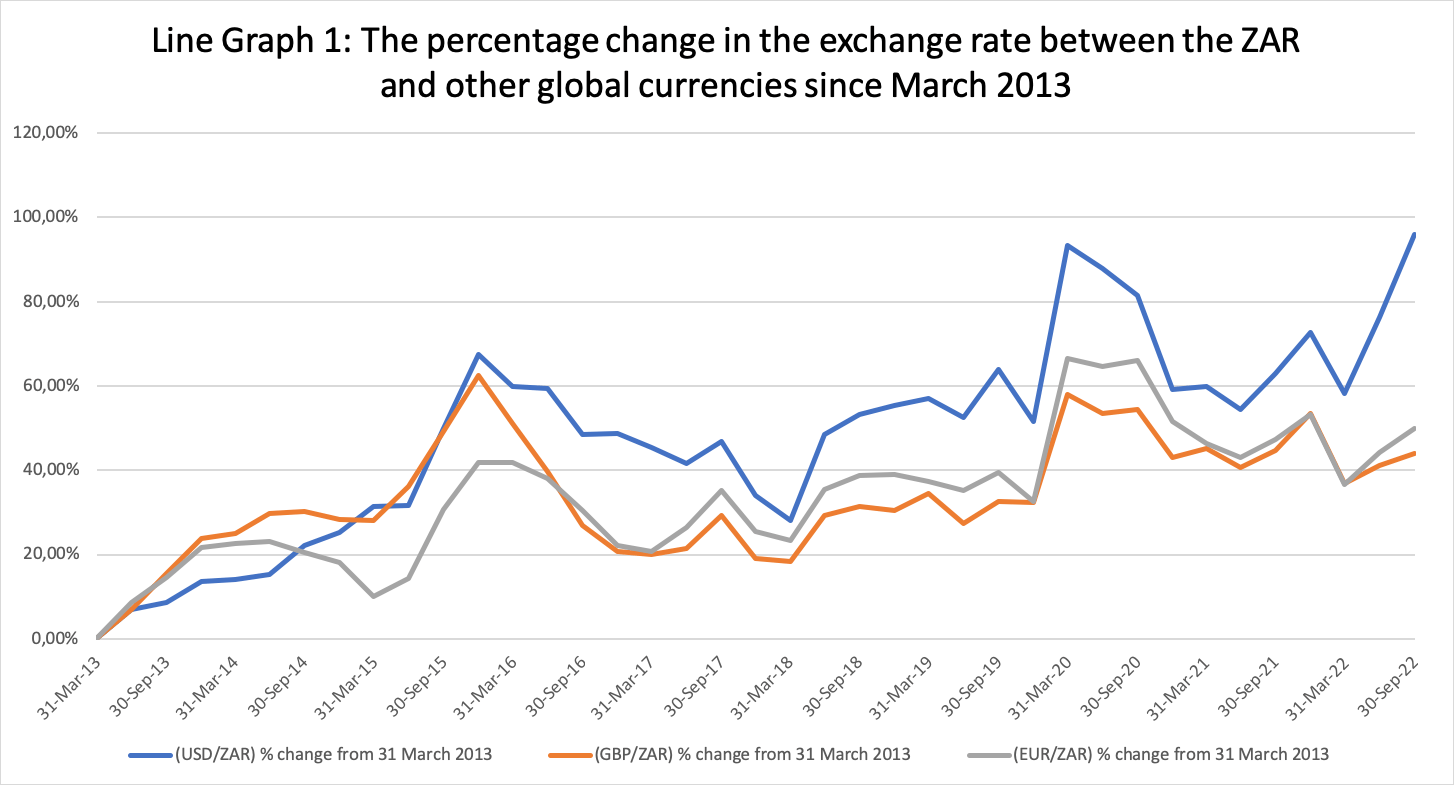

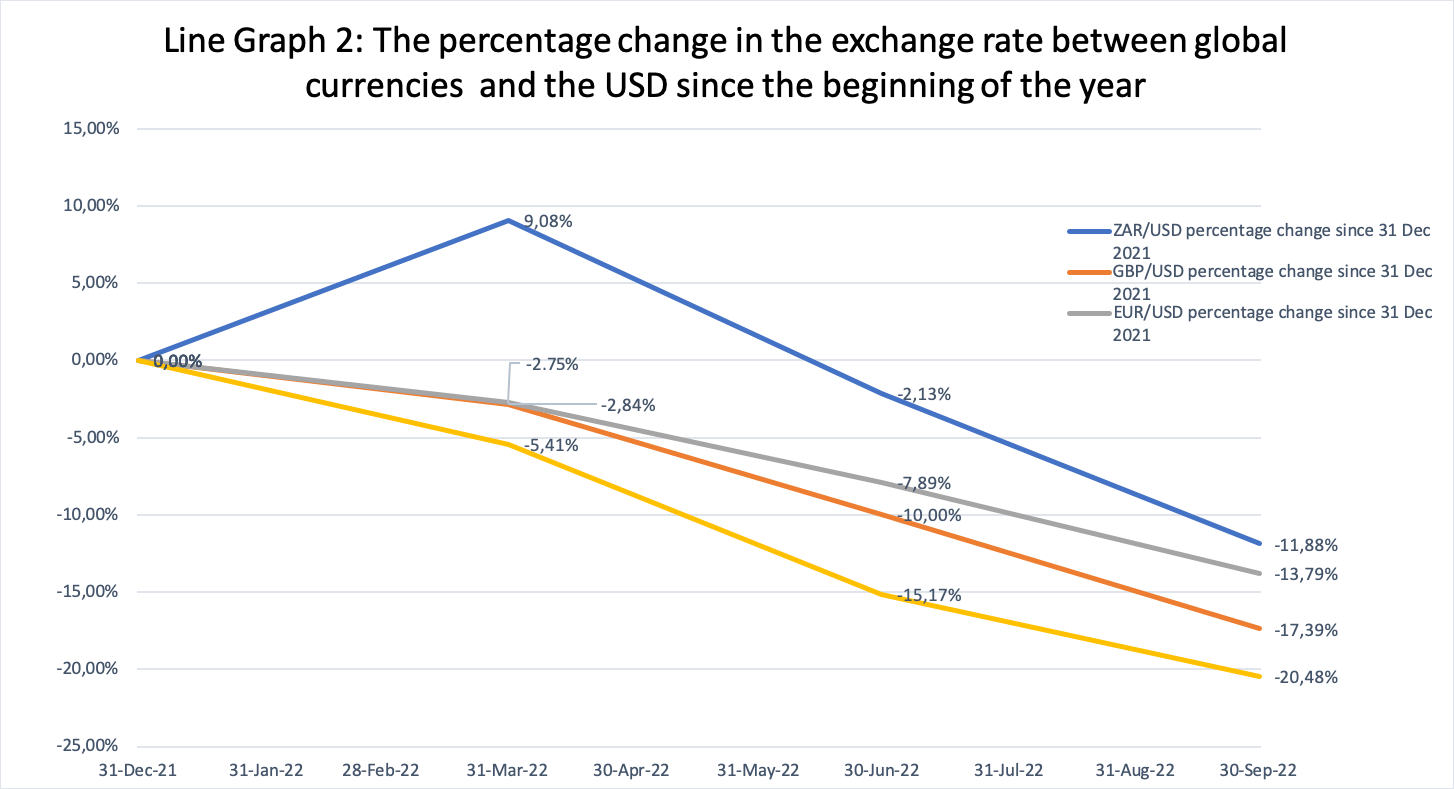

| USD/ZAR | 15,96 | 17,25 | 17,26 | 8,15% |

| EUR/ZAR | 17,95 | 17,86 | 17,82 | -0,72% |

| Brent Crude | 77,86 | 95,82 | 87,82 | 12,79% |

Source: iress

Lunar Capital on Eastwave Radio

Every Tuesday, at 07h45, Sabir chats with Nazia from Eastwave Radio (92.2 fm, live stream on www.eastwave.co.za) on investing and the markets.

Company and Market News

Last week, Walmart released their Q3 2022 results. Total revenue increased by 8.7% quarter on quarter to $152,8 billion. However, cost of sales increased at a higher rate of 10.1% to $115,6 billion. The higher cost of sales growth than revenue growth impacted Walmart’s gross margin, which decreased from 32,5% for Q3 2021 to 31,0% for the current quarter (Q3 2022). The gross margin of a company is a good indicator when looking at their ability to withstand the impact of inflation. The higher the gross margin, the better the company’s ability to withstand the impact of inflation. Despite the still high gross margin, Walmart registered a loss of $1,8 billion for the quarter largely because of opiod legal settlements. This is down from a profit of $3,1 billion for the same quarter last year. For the full fiscal year, Walmart expects year on year sales growth of 5,5%. They also expect fiscal year earnings per share to decline by 6% to 7% YoY. The share price for Walmart increased by 5,37% during the week.

Walmart were still able to grow sales in the current inflationary environment and they indicated that their share of higher income earners has increased as inflation and high fuel costs impact people’s buying power. In general, big retailers, such as Walmart are able to perform well when inflation is increasing. They are able to negotiate prices months before delivery (when inflation is lower.) And when they actually sell the goods, if prices for the goods are higher in the market, they are able to increase their prices accordingly.

Walmart faces competition from many different companies, including Amazon and Costco. These three companies try to gain market share by reducing their margins They can do this through the general way they set prices, or through loyalty programmes – which incentivise people to spend more but at discounted rates. Amazon does both of these, and they also have an additional super strength: their cloud business. Their cloud business has a much higher operating margin compared to the other segments of their business. Amazon are then able to subsidise their other businesses using the profits from their cloud segment.

Disclosure: Walmart and Amazon are held in the Lunar BCI Worldwide Flexible Fund.

Read our full Disclosure statement: https://lunarcapital.co.za/disclosures/

Our Privacy Notice: https://lunarcapital.co.za/privacy-policy/

The Lunar BCI Worldwide Flexible Fund Fact Sheet can be read here.

This roundup is prepared for the clients of Lunar Capital (Pty) Ltd. This roundup does not constitute financial advice and is generated for information purposes only.

Weekly Roundup 2022-11-18 – Walmart and Amazon Read More »