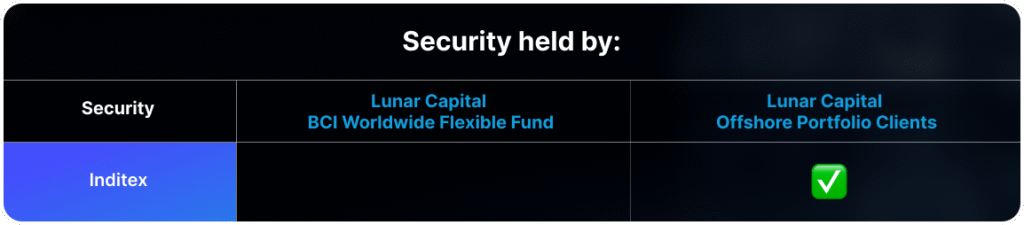

Last week, Inditex—the parent company of Zara—released its Q1 2025 results. Net sales for the quarter reached €8.2 billion, marking a modest 1.5% year-over-year increase. Net income rose to €1.3 billion, up 0.8% from the same period last year. While growth has slowed, largely due to market uncertainty surrounding tariffs, recessionary fears, and a strong euro. The company noted that in constant currency terms, sales would have increased by 4.2%.

Inditex’s hallmark is its highly flexible supply chain, which allows the company to adjust production in real time based on demand signals from both its online and physical stores.

This agility is particularly valuable during periods of economic uncertainty. With demand softening, Inditex is well-positioned to avoid excess inventory, reducing the risk of markdowns and impairments on its financial statements.

Since the COVID-19 pandemic, Inditex has been actively optimizing its store portfolio. The company has closed smaller, less productive stores while expanding larger ones and opening flagship locations in prime retail areas. This strategy has led to an increase in net sales per square metre, as customers tend to spend more when they can physically browse a broader selection of products.

Despite its focus on physical retail, Inditex continues to invest heavily in its e-commerce and logistics infrastructure. For FY24 and FY25, the company plans to allocate an additional €900 million annually in capital expenditure to enhance its logistics capabilities, supporting both online and offline growth.

Inditex maintains a strong financial position, with a net cash balance of €10.8 billion—down slightly from €11.6 billion in Q1 2024. This robust liquidity provides the company with significant strategic flexibility, enabling it to invest, expand, and navigate a market slowdown.

Click here to access your account to view statements, obtain tax certificates, add or make changes to your investments.

Our email address is: [email protected]

Disclosures

Lunar Capital (Pty) Ltd is a registered Financial Services Provider. FSP (46567)

Read our full Disclosure statement: https://lunarcapital.co.za/disclosures/

Our Privacy Notice: https://lunarcapital.co.za/privacy-policy/

The Lunar FR Worldwide Flexible Fund Fact Sheet can be read here.

This stocktake is prepared for the clients of Lunar Capital (Pty) Ltd. This stocktake does not constitute financial advice and is generated for information purposes only.