Who are you going to vote for?

Elections Everywhere Nigeria, Namibia, Indonesia, India, Spain, South Africa, …. Elections Everywhere. It seems like 2019 is the year of elections. As citizens, we are all interested and invested (in the broadest sense of the word) in the outcome of the election in South Africa, and maybe even in some other countries’ elections too. We […]

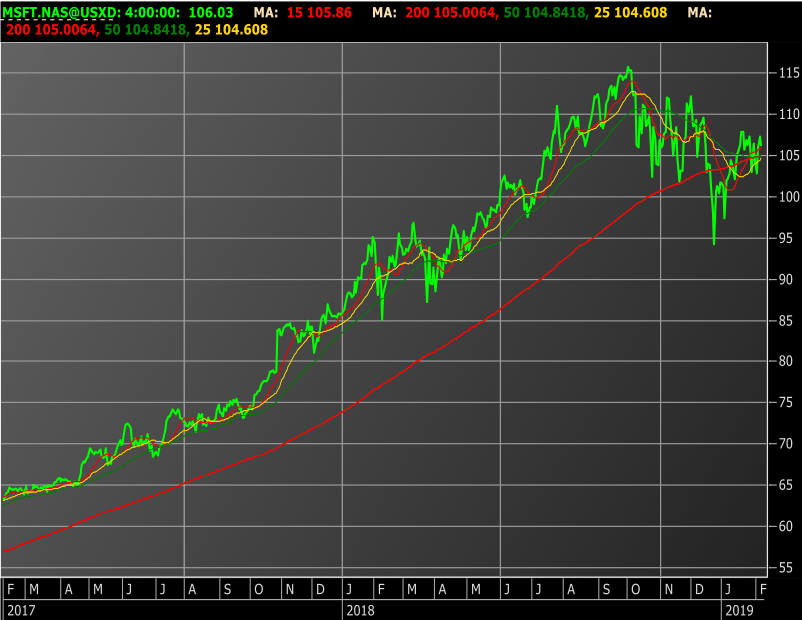

Share Focus: Microsoft (MSFT.NAS)

“Our strong commercial cloud results reflect our deep and growing partnerships with leading companies in every industry including retail, financial services, and healthcare,” said Satya Nadella, CEO of Microsoft. \”We are delivering differentiated value across the cloud and edge as we work to earn customer trust every day.” Microsoft’s mission is to empower every person […]

Time for a Rest

Listen to the podcast Transcript In a few days, many people will be taking some time off from work for their annual vacation. That is of course if they are fortunate enough to have a job. So, when I was thinking about this blog, several thoughts came to mind: Firstly, let’s do something different; […]

Good Markets, Bad Markets

Market Overview The market has been on a roller coaster ride over the last 3 months, showing good gains in August, but having a significant pull-back in September and October, both locally and offshore. The markets are largely driven by high valuations in the US; rising interest rates in the USA and Europe; and low […]

Active vs Passive

Market Overview A struggling local economy, flight of capital from emerging markets to developed markets, a volatile Rand and generally low or negative growth in company earnings have been the main drivers of the poor performance in the South African equity market. The Rand has weakened significantly against the major currencies (-12.8% YTD against the […]

Patience

View in PDF Market Overview The current market is characterised by political uncertainty and multiple global economic issues. The main issues affecting the South African market are Rand volatility, emerging market woes and political and policy uncertainty. The Rand has weakened significantly against the major currencies (-19.4% YTD against the USD) benefiting South African investors […]

What to do about the Rand?

[fusion_builder_container hundred_percent=\”no\” equal_height_columns=\”no\” menu_anchor=\”\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” class=\”\” id=\”\” background_color=\”\” background_image=\”\” background_position=\”center center\” background_repeat=\”no-repeat\” fade=\”no\” background_parallax=\”none\” parallax_speed=\”0.3\” video_mp4=\”\” video_webm=\”\” video_ogv=\”\” video_url=\”\” video_aspect_ratio=\”16:9\” video_loop=\”yes\” video_mute=\”yes\” overlay_color=\”\” video_preview_image=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” padding_top=\”\” padding_bottom=\”\” padding_left=\”\” padding_right=\”\”][fusion_builder_row][fusion_builder_column type=\”1_1\” layout=\”1_1\” background_position=\”left top\” background_color=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” border_position=\”all\” spacing=\”yes\” background_image=\”\” background_repeat=\”no-repeat\” padding=\”\” margin_top=\”0px\” margin_bottom=\”0px\” class=\”\” id=\”\” animation_type=\”\” animation_speed=\”0.3\” animation_direction=\”left\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” center_content=\”no\” last=\”no\” min_height=\”\” […]

Trade Wars

What is a Trade War? “A trade war is a side effect of protectionism that occurs when one country (Country A) raises tariffs on another country’s (Country B) imports in retaliation for Country B raising tariffs on Country A\’s imports. A tariff is a tax imposed on imported goods and services.” This is the definition […]

Share focus: NVIDIA

Nvidia manufactures high-end Graphical Processing Units (GPU’s) , i.e. computer processing chips. They work closely with software vendors that develop solutions on the Nvidia processors to build solutions for end-customers. Many AI (Artificial Intelligence), AV (Automated Vehicles); Cloud Computing Datacentres, and Gaming Applications utilise Nvidia processors. These are significant growth markets and the company has […]

Lunar BCI Worldwide Flexible Fund Two-Year Review

[fusion_builder_container hundred_percent=\”no\” equal_height_columns=\”no\” menu_anchor=\”\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” class=\”\” id=\”\” background_color=\”\” background_image=\”\” background_position=\”center center\” background_repeat=\”no-repeat\” fade=\”no\” background_parallax=\”none\” parallax_speed=\”0.3\” video_mp4=\”\” video_webm=\”\” video_ogv=\”\” video_url=\”\” video_aspect_ratio=\”16:9\” video_loop=\”yes\” video_mute=\”yes\” overlay_color=\”\” video_preview_image=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” padding_top=\”\” padding_bottom=\”\” padding_left=\”\” padding_right=\”\”][fusion_builder_row][fusion_builder_column type=\”1_1\” layout=\”1_1\” background_position=\”left top\” background_color=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” border_position=\”all\” spacing=\”yes\” background_image=\”\” background_repeat=\”no-repeat\” padding=\”\” margin_top=\”0px\” margin_bottom=\”0px\” class=\”\” id=\”\” animation_type=\”\” animation_speed=\”0.3\” animation_direction=\”left\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” center_content=\”no\” last=\”no\” min_height=\”\” […]