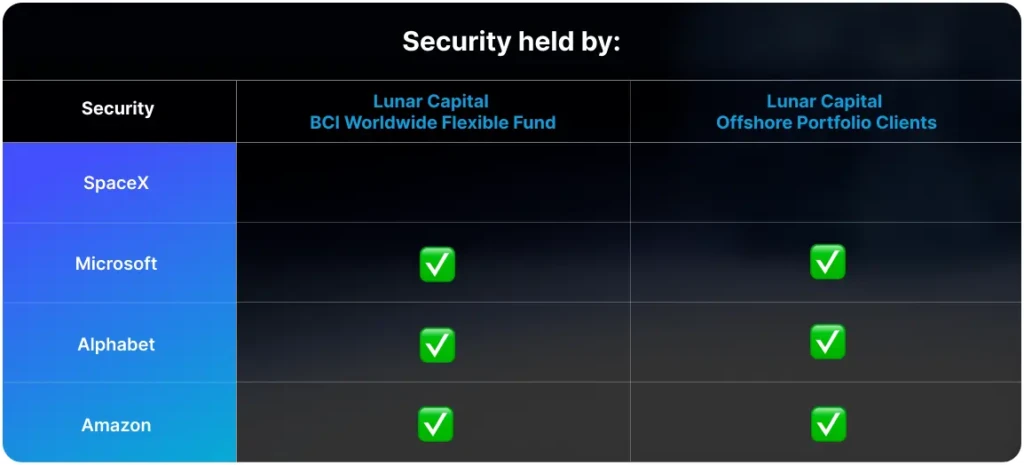

SpaceX’s long-awaited IPO has arrived with historic force. The company raised approximately $75 billion in what is now the largest IPO in history, valuing the business at close to $1.8 trillion as of Friday. In the process, Elon Musk, who retains roughly 42% ownership, has effectively become the world’s first trillionaire.

With companies like Anthropic and OpenAI reportedly eyeing public markets, SpaceX’s success signals that investor appetite for large, narrative-driven technology listings remains firmly intact. Companies tend to go public when market conditions are most favourable. Elevated valuations and strong liquidity allow businesses to raise significant capital while diluting less equity than they otherwise would in more subdued markets.

There are clear signs that this dynamic was at play. Retail demand alone exceeded $100 billion, though individual investors ultimately received only around 20–25% of the allocated shares. The bulk went to sovereign wealth funds, pension funds, and large asset managers.

SpaceX is positioning itself as a platform for multiple future industries. The company plans to deploy IPO proceeds across an ambitious set of projects, including its Starship rocket programme, a proposed million-person Mars colony, a future lunar economy, and orbital AI data centres capable of delivering computing capacity from space.

These ambitions are undeniably bold, but they highlight a key concern. Most of these industries do not yet exist in any meaningful commercial form. Their success is uncertain, the timelines are long, and the capital requirements are enormous. While the IPO prospectus references a $28.5 trillion addressable market, this figure is largely theoretical and depends on markets being created, rather than simply captured.

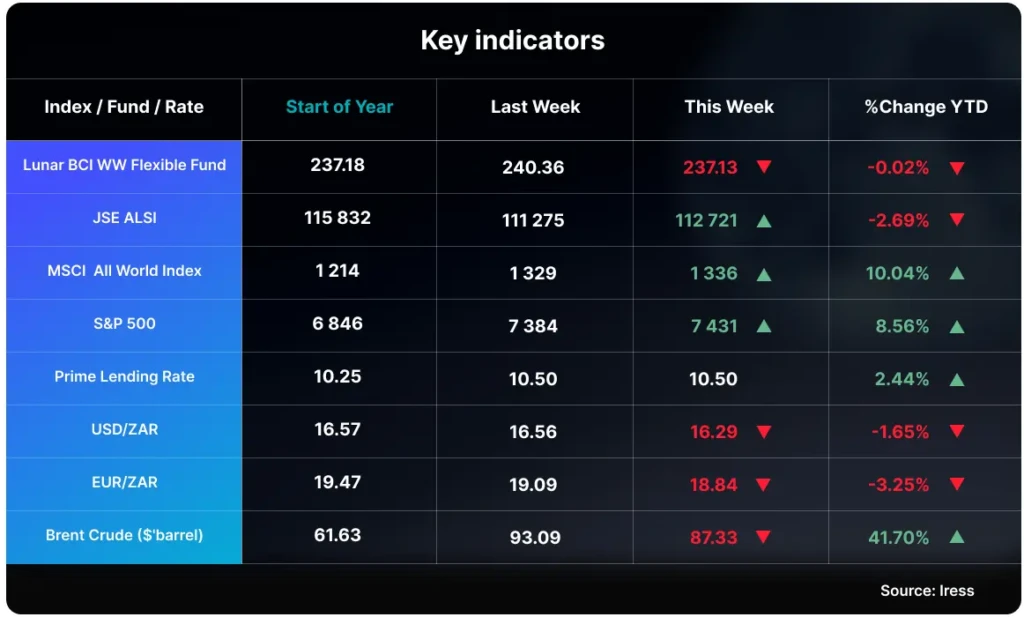

At its current valuation, SpaceX is trading at over 100 times last year’s revenue. For context, Amazon trades at a fraction of that multiple, around 3.7 times revenue and 29 times earnings. SpaceX generated $18.7 billion in revenue last year while posting a loss of $4.9 billion, reinforcing the gap between valuation and current financial performance.

The company’s AI initiatives also raise questions. Unlike peers such as Microsoft, Amazon, and Alphabet, where demand for AI infrastructure continues to exceed supply, SpaceX appears to have excess compute capacity, to the point where it is leasing some of it out to companies like Alphabet and Anthropic.

In the near term, the stock may benefit from favourable technical dynamics. Over the coming weeks, passive index funds tracking major benchmarks such as the Nasdaq, FTSE, and MSCI are likely to begin purchasing shares following SpaceX’s fast-tracked inclusion. This will bring millions of pension savers and holders of passive instruments into the shareholder base indirectly.

Click here to access your account to view statements, obtain tax certificates, add or make changes to your investments.

Our email address is: [email protected]

Disclosures

Lunar Capital (Pty) Ltd is a registered Financial Services Provider. FSP (46567)

Read our full Disclosure statement: https://lunarcapital.co.za/disclosures/

Our Privacy Notice: https://lunarcapital.co.za/privacy-policy/

The Lunar FR Worldwide Flexible Fund Fact Sheet can be read here.

This stocktake is prepared for the clients of Lunar Capital (Pty) Ltd. This stocktake does not constitute financial advice and is generated for information purposes only.