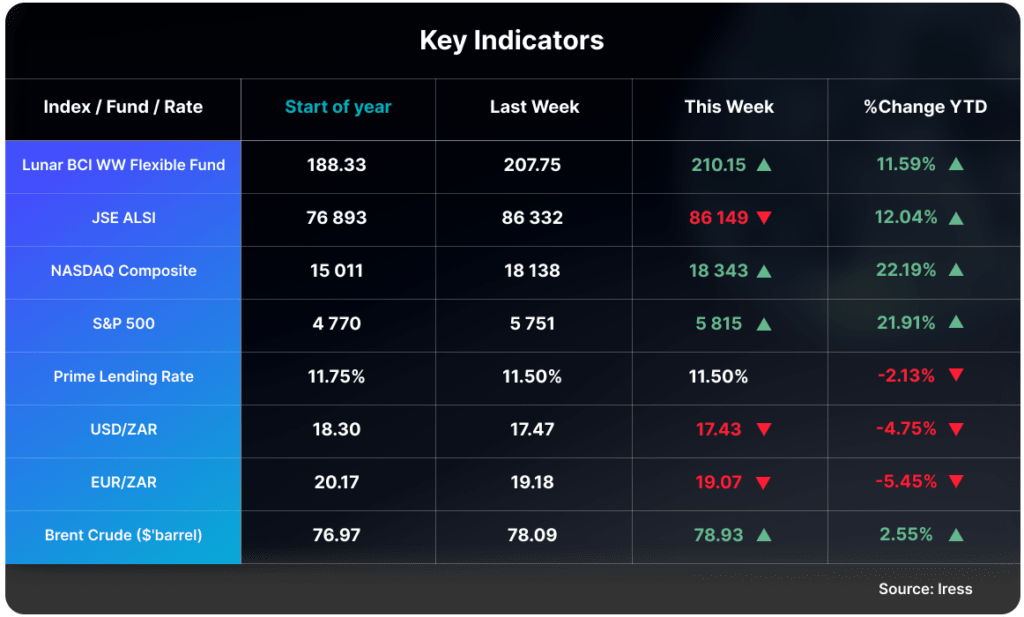

JP Morgan, known for its fortress balance sheet, released its Q3 2024 results on Friday. The bank reported net revenues of $42.7 billion, representing a 7% year-over-year increase. Net income for JP Morgan was $12.9 billion, a decline of 2% compared to the previous year. The bank’s return on equity (ROE) for the quarter stood at 16%. This was partly driven by efficiencies from tech investments and lazy deposits (customers who settled for lower returns on their deposits than they would get in other accounts.)

The discrepancy between the rise in net revenue and the decline in net income was attributed to higher provisions for credit losses, which amounted to $3.1 billion, an increase of 125% from the same period last year. Despite this, JP Morgan’s balance sheet is well-positioned to withstand such financial pressures.

Following the 2008 Global Financial Crisis, the Basel III framework was introduced to enhance banking regulation. One significant part of the regulation requires banks to maintain a common equity tier 1 (CET 1) ratio of at least 4.5%. Regulators may require higher ratios from specific banks. The CET 1 ratio reflects a bank’s core capital, comprising common shares, retained earnings, and additional paid-in capital. It is considered the most secure form of capital, essential for enhancing a bank’s financial resilience and safeguarding depositors during financial shocks. JP Morgan’s CET1 ratio is 15.3% on risk weighted assets of USD1.8tn, giving it an estimated loss-absorbing capacity of USD544bn.

With such a large asset and capital base, and broad product suite; JP Morgan services over 82 million US consumers, 6 million small businesses and 40 thousand large- and medium businesses around the world. JP Morgan’s strong balance sheet also allows it to take advantage of growth opportunities when the market goes through a downturn.

Click here to access your account to view statements, obtain tax certificates, add or make changes to your investments.

Our email address is: [email protected]

Disclosures

Lunar Capital (Pty) Ltd is a registered Financial Services Provider. FSP (46567)

Read our full Disclosure statement: https://lunarcapital.co.za/disclosures/

Our Privacy Notice: https://lunarcapital.co.za/privacy-policy/

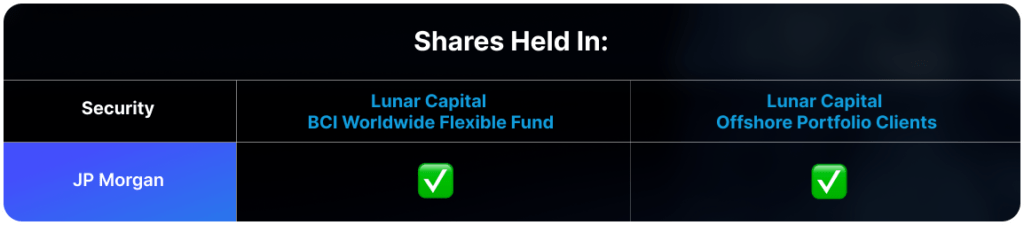

The Lunar BCI Worldwide Flexible Fund Fact Sheet can be read here.

This stocktake is prepared for the clients of Lunar Capital (Pty) Ltd. This stocktake does not constitute financial advice and is generated for information purposes only.