In 1998, Compaq Research introduced the first “Personal Jukebox.” Although the device was bulky and could only store the equivalent of one CD, it represented a significant advancement in portable music technology. Recognizing its potential, Apple procured exclusive rights to affordable 5GB disc drives developed by Toshiba, which were capable of storing up to 1,000 songs. Apple subsequently redesigned the media player with a sleek and user-friendly interface and launched the iPod in 2001.

Apple is known for observing market trends before developing its own products. The company waits to see which products become popular and, if there is potential for further growth, it creates its own versions with Apple’s distinctive design and sells them to the market.

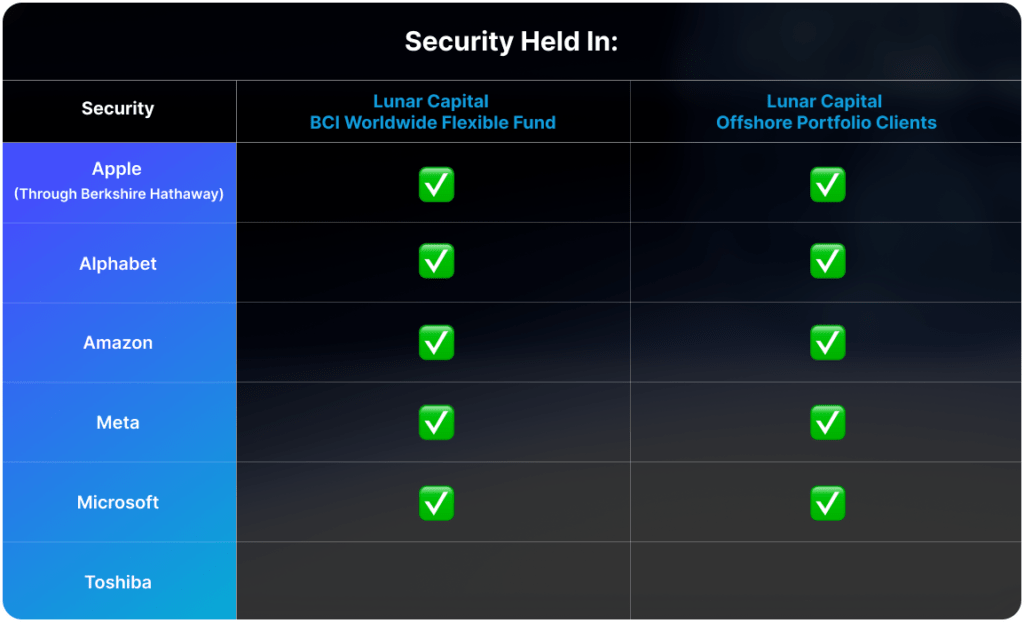

In the realm of generative AI, Apple has taken a unique approach compared to other major technology companies like Alphabet, Amazon, Meta, and Microsoft. Unlike these firms, Apple has not significantly increased its capital expenditure on building data centres.

Instead, Apple opted for its more patient strategy, aiming to develop an AI of the highest quality. Initially, this method presented some challenges for Apple, such as delays and bugs in the AI features on its devices. Now, in cases where Apple’s AI is unable to generate responses for users, it utilizes ChatGPT to provide the necessary responses.

Apple’s strength lies in its highly valuable consumer distribution platform, designed to create a seamless experience for users centred around the iPhone. In Q4 2024, Apple’s products and services generated a revenue of $124 billion, with an operating income of $42 billion. This robust distribution to a highly valuable customer base is a key strength and could position Apple as one of the significant beneficiaries in the AI race.

Click here to access your account to view statements, obtain tax certificates, add or make changes to your investments.

Our email address is: [email protected]

Disclosures

Lunar Capital (Pty) Ltd is a registered Financial Services Provider. FSP (46567)

Read our full Disclosure statement: https://lunarcapital.co.za/disclosures/

Our Privacy Notice: https://lunarcapital.co.za/privacy-policy/

The Lunar BCI Worldwide Flexible Fund Fact Sheet can be read here.

This stocktake is prepared for the clients of Lunar Capital (Pty) Ltd. This stocktake does not constitute financial advice and is generated for information purposes only.