Snowflake is a company that provides a platform which enables businesses and organisations to organise and share data across multiple cloud environments. Recently, the company has been shifting its focus toward helping customers leverage their data for artificial intelligence (AI) applications.

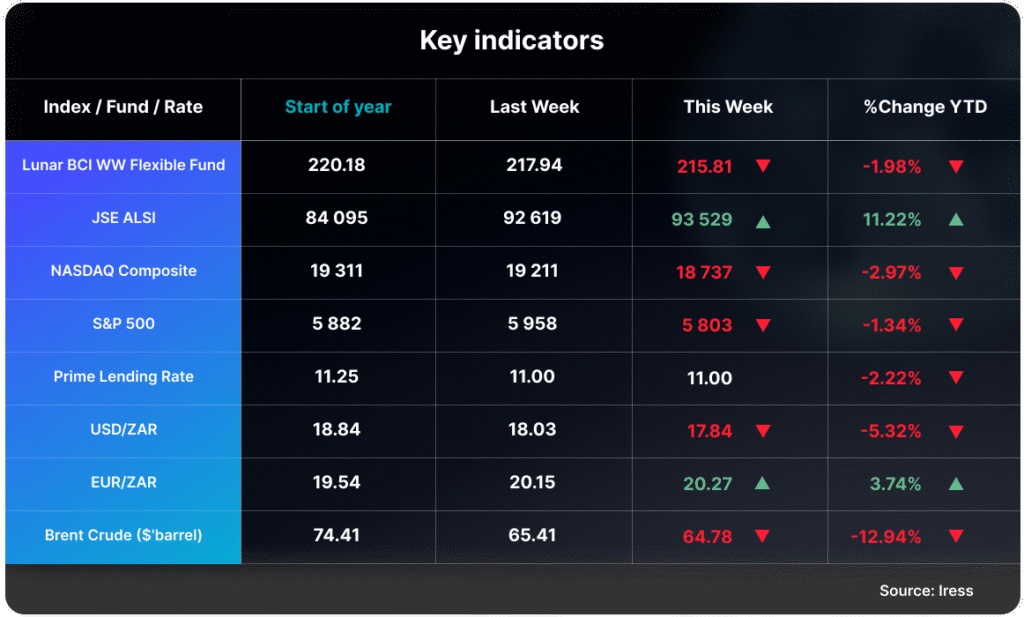

Last week, Snowflake reported its financial results for the first quarter of fiscal year 2026. Revenue for the quarter reached $1 billion, representing a 26% increase year over year. However, the company also reported an operating loss of $447 million, up 28% from the same period last year.

Snowflake has observed a shift in its customer base since the COVID-19 pandemic. During the pandemic, its primary customers were startups that spent aggressively on cloud services. In contrast, the current customer base consists largely of larger, more cost-conscious organisations with stricter budget controls. As of the latest quarter, Snowflake serves 754 companies from the Forbes Global 2000 list and has 606 customers that each generated over $1 million in revenue over the past 12 months.

Despite strong revenue growth and a solid customer base, Snowflake faces challenges as it continues to scale. Like many smaller publicly listed companies, Snowflake uses stock-based compensation to attract and retain talent, as it may not be able to match the cash compensation offered by larger technology firms. However, this approach can lead to shareholder dilution, as it increases the total number of shares outstanding.

In Q1 2026, stock-based compensation accounted for just over 40% of Snowflake’s revenue; its operating margin was also -44%. The company managed to keep the total number of shares roughly in line with the same quarter last year by repurchasing shares from existing shareholders using its cash reserves. While this strategy helps offset dilution, it carries the risk of inefficient capital allocation, especially if shares are repurchased at high valuations.

Snowflake has demonstrated consistent revenue growth in recent years. However, its increasing reliance on stock-based compensation to support this growth may become a concern for investors if not addressed.

Click here to access your account to view statements, obtain tax certificates, add or make changes to your investments.

Our email address is: [email protected]

Disclosures

Lunar Capital (Pty) Ltd is a registered Financial Services Provider. FSP (46567)

Read our full Disclosure statement: https://lunarcapital.co.za/disclosures/

Our Privacy Notice: https://lunarcapital.co.za/privacy-policy/

The Lunar FR Worldwide Flexible Fund Fact Sheet can be read here.

This stocktake is prepared for the clients of Lunar Capital (Pty) Ltd. This stocktake does not constitute financial advice and is generated for information purposes only.