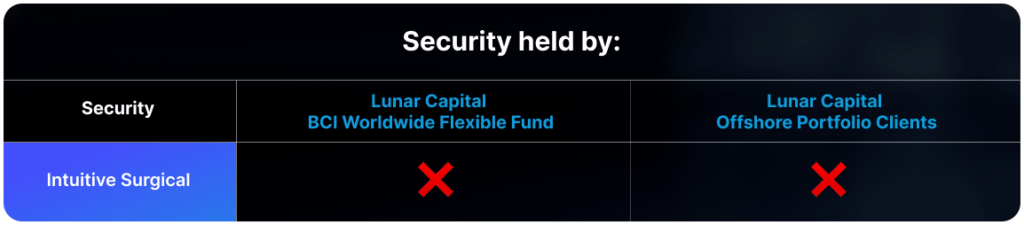

Intuitive Surgical, a leading developer of robotic-assisted surgery systems, reported solid growth in its latest quarterly results while acknowledging rising competitive pressures. The Californian company, best known for its da Vinci surgical tool, has established itself as a key player in minimally invasive procedures across urology, gynaecology and general surgery.

For the fourth quarter of 2025, revenue rose 19 per cent year on year to $2.87bn, with net income increasing 15 per cent to $795m. The da Vinci 5, cleared by the US Food and Drug Administration in March 2024, has been an important contributor. Its Force Feedback Technology, which enables surgeons to sense pressure at the instrument tip, has been associated with reduced tissue trauma and improved patient outcomes.

System placements reached 532 in the quarter. That compares with 493 a year earlier. The installed base rose to 11,106 units by the end of December, representing a 12 per cent increase. Procedure volumes expanded by 18 per cent globally. Growth was supported by both the da Vinci system and the ION endoluminal platform. Cardiac procedures accounted for about 17,000 during the quarter.

Revenue composition reflects a recurring model: system sales contributed 29 per cent, while accessories and consumables required for each procedure made up 61 per cent. This structure has provided resilience. However, the company noted increasing competition in international market, especially from Chinese manufacturers. Local rivals in China have introduced systems with architectures similar to the previous da Vinci Tool. They have also pursued aggressive pricing strategies, affecting Intuitive’s win rates in certain tenders.

Intuitive’s shares trade at a price-to-earnings ratio of 66. The company said they expect procedure growth for the da Vinci 5 of between 13% and 15%, below some market forecasts. Shares have declined about 6 per cent year to date, reflecting concerns that growth may be moderating as competition intensifies.

Click here to access your account to view statements, obtain tax certificates, add or make changes to your investments.

Our email address is: [email protected]

Disclosures

Lunar Capital (Pty) Ltd is a registered Financial Services Provider. FSP (46567)

Read our full Disclosure statement: https://lunarcapital.co.za/disclosures/

Our Privacy Notice: https://lunarcapital.co.za/privacy-policy/

The Lunar FR Worldwide Flexible Fund Fact Sheet can be read here.

This stocktake is prepared for the clients of Lunar Capital (Pty) Ltd. This stocktake does not constitute financial advice and is generated for information purposes only.