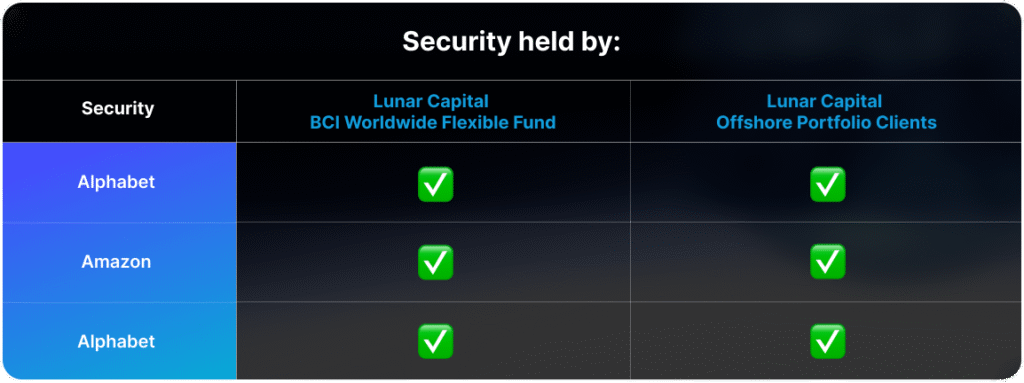

In Q3 2025, Alphabet, Microsoft, and Amazon demonstrated their deep commitment to artificial intelligence through aggressive investment and infrastructure expansion. Alphabet reported $102.3 billion in revenue, with AI driving growth across Google Cloud and consumer products. Over 650 million users engage with its Gemini model, and nearly half the code generated for Google products is now AI-generated. Google Cloud’s $155 billion backlog, up 82% year over year, shows an ever-increasing demand. Alphabet is continuing to increase their capital expenditure (CapEx). Alphabet plans to spend $75billion to $85 billion in capital expenditure this year.

Microsoft posted $77.7 billion in revenue and $38 billion in operating profit, with Azure growing 40% year over year. Its $392 billion commercial remaining performance obligation signals robust future demand. CapEx rose 74% to $34.9 billion, with half spent on short-lived GPU assets. Microsoft finances 44% of CapEx through leases. Microsoft is expanding its data center footprint around the world to meet sovereign requirements. The pace of spending, especially on rapidly depreciating hardware such as GPUs, poses risks if demand softens. However, the company is building out its infrastructure in a way that gives them flexibility in how they utilise their infrastructure. If demand drops in one area the infrastructure can be used in another area.

Amazon reported $180.2 billion in net sales, with AWS contributing $33 billion. They have a backlog of $200 billion, excluding the announcement post their results presentation of a $38bn deal to supply OpenAI with capacity.. AI infrastructure expanded by 3.8 GW, with plans to double overall capacity by 2027. Q3 CapEx reached $34.2 billion, with full-year estimates at $125 billion. Its Tranium chip business grew 150% quarter over quarter, and Tranium 2 is fully subscribed. Amazon’s strategy of offering both custom and NVIDIA chips provides flexibility. Amazon is also investing aggressively in its ecommerce fulfilment business. The company incurred Federal Trade Commission fines in the US. They also announced a restructuring to cut 15% of its corporate workforce, to reduce corporate bureacracy. This has resulted in their operating income remaining flat year over year.

Collectively, these companies are building the backbone of the AI economy, but the risks of overspending on CapEx are real. With billions committed to infrastructure, the pressure to deliver returns, manage depreciation, and adapt to fast-moving technological change will define their success in the AI era.

Click here to access your account to view statements, obtain tax certificates, add or make changes to your investments.

Our email address is: [email protected]

Disclosures

Lunar Capital (Pty) Ltd is a registered Financial Services Provider. FSP (46567)

Read our full Disclosure statement: https://lunarcapital.co.za/disclosures/

Our Privacy Notice: https://lunarcapital.co.za/privacy-policy/

The Lunar FR Worldwide Flexible Fund Fact Sheet can be read here.

This stocktake is prepared for the clients of Lunar Capital (Pty) Ltd. This stocktake does not constitute financial advice and is generated for information purposes only.