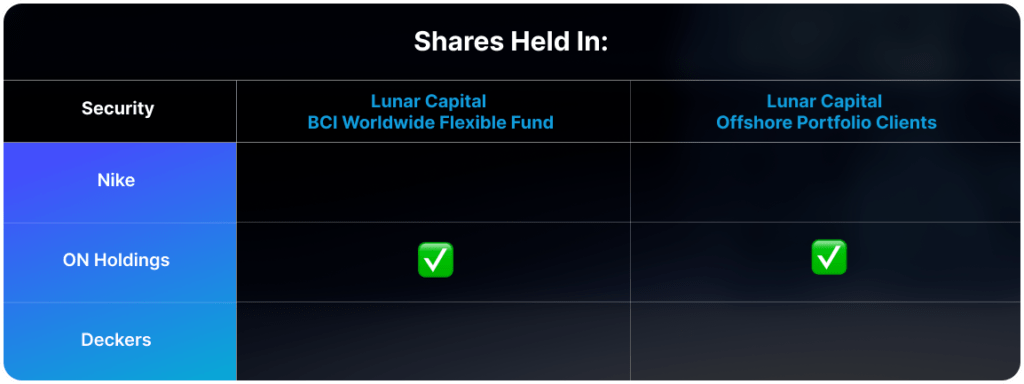

Nike, which was expected to be ideally positioned for “running mania”, released its Q1 2025 results. Revenue for the quarter declined by 10% year-over-year, reaching $11.6 billion. Gross margin improved by 120 basis points to 45.4%, while net profits fell by 26%, amounting to $1.05 billion. Nike’s share price has dropped over 22% this year and more than 50% since its peak in November 2021.

Nike, renowned for its innovative products, memorable advertising campaigns, and strong athlete partnerships, has been losing market share to both established and emerging brands such as New Balance, On, and Hoka.

Under the previous CEO, John Donahoe, the company concentrated on expanding its direct-to-consumer business model. This included increasing capacity for its e-commerce channel and further developing Nike-run stores. The goal was to gain better control over sales and improve the bottom line by avoiding consignment fees to wholesale retailers. However, this strategy strained relationships with wholesale partners, leading some to remove Nike products from their stores.

This approach seemed adequate during the COVID-19 pandemic when online shopping surged. However, as demand for Nike’s products began to decline, the company struggled to maintain growth.

The new CEO, Elliott Hill, has placed a strong emphasis on mending relationships with wholesale partners and acknowledged that Nike had deviated from its core strengths of product innovation and designing athletic footwear. Hill believes that that Nike will only be able to generate strong demand for their lifestyle products after they accomplish the feat of designing great athletics wear.

While turnarounds are challenging to implement, especially in a highly competitive fashion and high-performance sports sector, Nike possesses a relatively strong balance sheet with $8.5 billion in cash. Time will determine if they can Do It.

Click here to access your account to view statements, obtain tax certificates, add or make changes to your investments.

Our email address is: [email protected]

Disclosures

Lunar Capital (Pty) Ltd is a registered Financial Services Provider. FSP (46567)

Read our full Disclosure statement: https://lunarcapital.co.za/disclosures/

Our Privacy Notice: https://lunarcapital.co.za/privacy-policy/

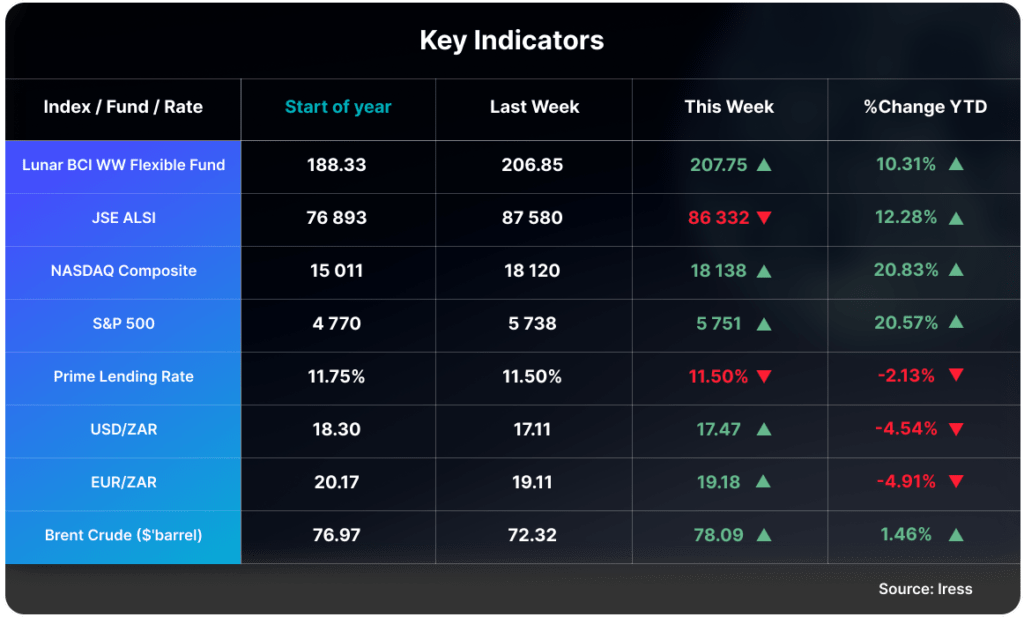

The Lunar BCI Worldwide Flexible Fund Fact Sheet can be read here.

This stocktake is prepared for the clients of Lunar Capital (Pty) Ltd. This stocktake does not constitute financial advice and is generated for information purposes only.