Netflix delivered a strong start to its 2026 financial year, posting solid growth even as investors reacted cautiously to the results.

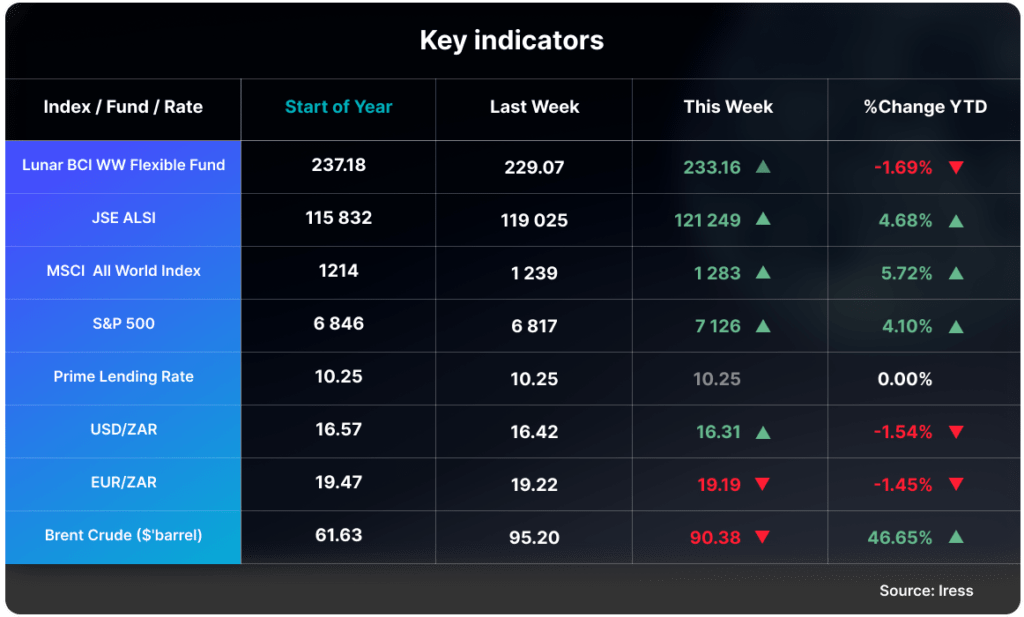

For the first quarter, the streaming giant reported revenue of $12.3 billion, up 16.2% year on year. Profitability also continued to improve, with operating margins rising to 32.3%, reflecting the operating leverage Netflix has built as its subscriber base and advertising business scale. Despite these numbers, the company’s share price fell by about 10% after the results, largely due to high expectations already embedded in the valuation and the pace of future earnings growth.

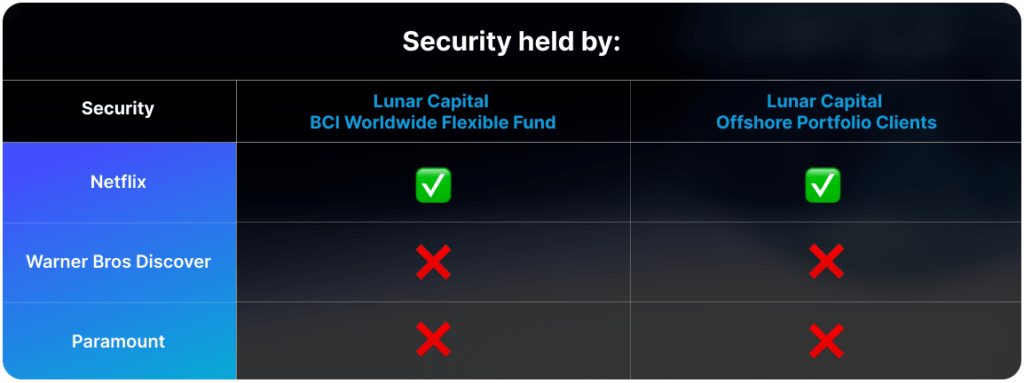

One of the biggest strategic updates was Netflix’s decision to walk away from a potential acquisition of Warner Brothers. After Paramount made a counteroffer that was accepted, Netflix exited the process, with Paramount agreeing to cover the $2.8 billion breakup fee. Management reiterated that walking away was about protecting shareholder value, while also reaffirming its long held preference for building content and capabilities internally rather than pursuing large, transformative acquisitions. That said, Netflix remains open to opportunistic deals where these make strategic sense.

The company’s advertising push continues to gain momentum. Netflix’s ad-supported tier has become the primary source of new subscriptions, helping its advertising business generate $1.5 billion in revenue during 2025, still a relatively low percentage of overall revenue. Management has indicated ambitions to double that figure to $3 billion in 2026. The advertising base expanded by 70% year on year, now reaching over 4 000 advertisers.

Beyond traditional series and films, Netflix is investing more aggressively in new content formats to increase engagement. Live sports are playing an increasingly meaningful role, with the World Baseball Classic becoming Netflix’s most-watched program ever in Japan. The company is also ramping up its investment in podcasts, a move that has had an interesting side effect: viewers are spending more time on the platform during the day, shifting usage away from the traditional evening peak.

Leadership changes are also on the horizon. Founder and executive chair Reed Hastings will step down at the end of his current term, marking the end of an era for the company he helped build into a global streaming powerhouse.

Finally, Netflix addressed its approach to artificial intelligence, a topic drawing growing attention across the entertainment industry. Management emphasized that AI is intended to support, not replace, creative talent. The current focus is on preproduction tools such as idea generation and storyboarding, aimed at improving efficiency and helping creators bring better ideas to the screen.

Overall, Netflix’s quarter underscored a business still growing strongly, broadening its revenue base, and experimenting with new formats, even as the market weighs how much of that success is already reflected in its share price.

Click here to access your account to view statements, obtain tax certificates, add or make changes to your investments.

Our email address is: [email protected]

Disclosures

Lunar Capital (Pty) Ltd is a registered Financial Services Provider. FSP (46567)

Read our full Disclosure statement: https://lunarcapital.co.za/disclosures/

Our Privacy Notice: https://lunarcapital.co.za/privacy-policy/

The Lunar FR Worldwide Flexible Fund Fact Sheet can be read here.

This stocktake is prepared for the clients of Lunar Capital (Pty) Ltd. This stocktake does not constitute financial advice and is generated for information purposes only.