On Holdings, owners of the On Cloud sports brand best known for its distinctive running shoes, recently released its Q2 2024 results. The company reported a revenue of CHF 567.7 million, marking a 28% increase year-over-year. Operating income rose by 20% to CHF 47.3 million. The brand has a strong presence in the U.S., where 65% of last quarter’s sales originated, showing a growth of over 24% compared to the same period last year. Although the Asia-Pacific region was the fastest-growing market with nearly 74% growth, it only accounted for 10% of the company’s net sales for the quarter.

The bulk of On Holdings’ revenue (95%) comes from its shoe sales, which grew by nearly 27% year-over-year. As a relatively small brand compared to giants like Nike and Adidas, On Holdings faces both opportunities and challenges. The company has significant potential for growth by expanding into new regions and diversifying its product range.

One of On Holdings’ recent innovations is a new shoe that is sprayed onto a person’s foot, weighing just 158g for the women’s version. Helen Obiri, a renowned Kenyan middle- and long-distance runner, trained in these shoes for the recent Olympics and was so impressed that she wore them during the Paris Olympics marathon, where she won a bronze medal. This reflects On Holdings’ strategy of collaborating with athletes to design products that cater specifically to their sports.

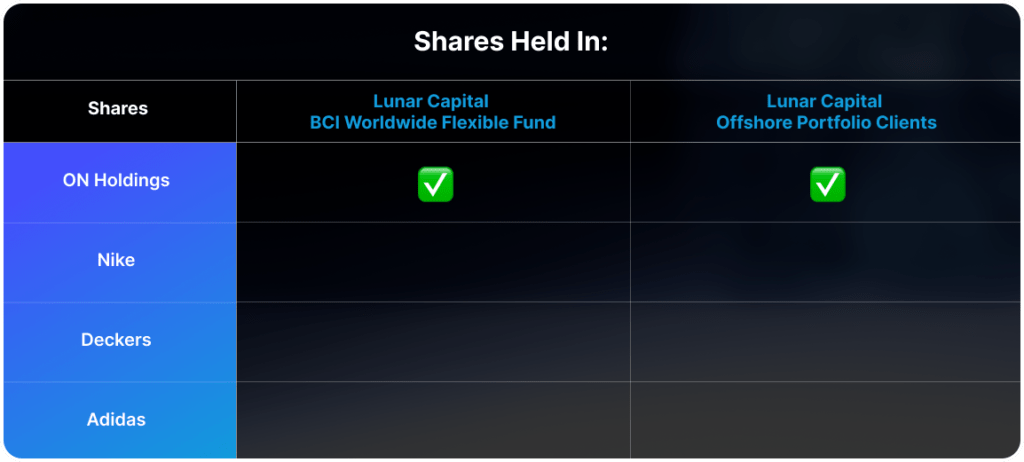

On Holdings does however operate in a highly competitive market, facing rivals ranging from smaller brands like Deckers, which owns the popular Hoka brand, to industry giants like Nike and Adidas. Fashion trends can shift rapidly, and consumer preferences are fickle, posing a constant challenge. For now, On Holdings is capitalizing on current trends, but the landscape could change quickly.

Click here to access your account to view statements, obtain tax certificates, add or make changes to your investments.

Our email address is: [email protected]

Disclosures

Lunar Capital (Pty) Ltd is a registered Financial Services Provider. FSP (46567)

Read our full Disclosure statement: https://lunarcapital.co.za/disclosures/

Our Privacy Notice: https://lunarcapital.co.za/privacy-policy/

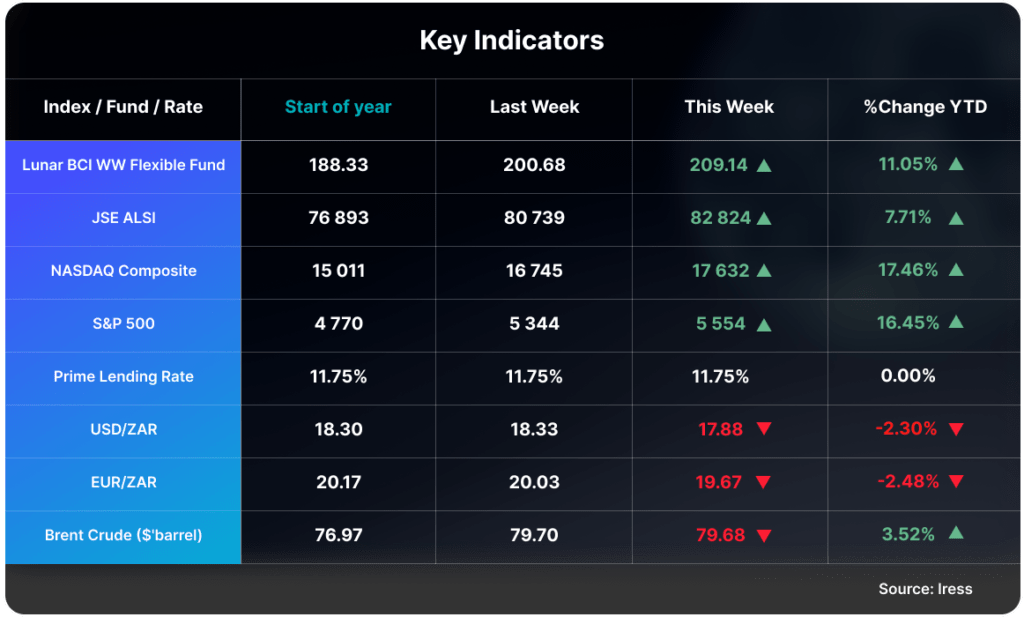

The Lunar FR Worldwide Flexible Fund Fact Sheet can be read here.

This stocktake is prepared for the clients of Lunar Capital (Pty) Ltd. This stocktake does not constitute financial advice and is generated for information purposes only.