Mercado Libre (Meli) has become one of the most important digital platforms in Latin America by building an ecosystem that tightly integrates ecommerce, payments, logistics, credit and advertising. The company operates across 18 countries, with their strongest positions in Brazil, Mexico and Argentina. One of its biggest advantages is the way its products reinforce the others, creating a flywheel that continues to drive growth as the platform expands.

That flywheel was evident in the company’s Q4 2025 results. Net revenue reached $8.8 billion, up 45% year over year, extending Mercado Libre’s streak to 28 consecutive quarters of revenue growth above 30%. At this scale, such consistency highlights both the structural under-penetration of ecommerce and digital financial services in the region; and the company’s ability to execute across multiple verticals simultaneously. Operating income rose to $889 million, with a margin of 10.1%, down 340 basis points from the prior year. This compression reflects a deliberate decision to prioritise growth and market-share gain over near-term profitability.

The ecommerce business generated $4.98 billion in revenue, growing 37% year over year, while unique active buyers increased 24% to 83 million. Initiatives such as free shipping on low value items in Brazil have reduced friction for first-time buyers and driven higher purchase frequency across more categories.

Fintech continues to be the most powerful growth engine within the ecosystem. Mercado Pago delivered revenue of $3.78 billion, up 61% year over year, with total payment volume rising 42% to $83.7 billion. Monthly active fintech users grew 67% to 78 million, underscoring the platform’s evolution from a payments tool into a primary financial account for many users. Attractive yields on wallet balances have also supported strong retention, giving customers little reason to use external saving accounts.

The interaction between commerce and fintech businesses remains central to Meli’s push to gain market share. Transaction data from the ecommerce marketplace enhances the company’s ability to price risk and extend credit to both consumers and merchants. Improved access to credit drives higher transaction volumes, which in turn feeds payments growth, data generation and monetisation across the platform.

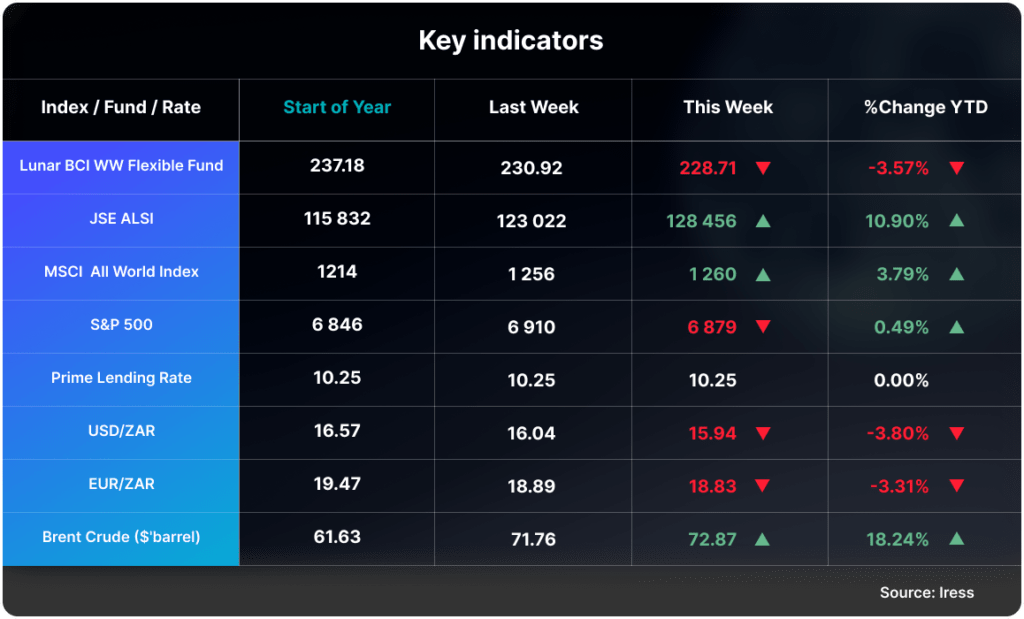

At a PE ratio of 48.8, Mercado Libre is priced to continue growing at elevated level. The positioning comes with risk. The stock is volatile due to exposure to multiple Latin American currencies, macro and political uncertainty, and its classification as an emerging market business. Earnings can be materially affected by foreign exchange movements and inflation dynamics outside management’s control. Volatility is further amplified by management’s willingness to prioritise long-term investment over short-term profitability, which can result in margin compression and uneven quarterly results.

Click here to access your account to view statements, obtain tax certificates, add or make changes to your investments.

Our email address is: [email protected]

Disclosures

Lunar Capital (Pty) Ltd is a registered Financial Services Provider. FSP (46567)

Read our full Disclosure statement: https://lunarcapital.co.za/disclosures/

Our Privacy Notice: https://lunarcapital.co.za/privacy-policy/

The Lunar FR Worldwide Flexible Fund Fact Sheet can be read here.

This stocktake is prepared for the clients of Lunar Capital (Pty) Ltd. This stocktake does not constitute financial advice and is generated for information purposes only.