Exposure to cutting-edge global businesses

Timothy Rangongo from finweek reviewed the Lunar FR Worldwide Flexible Fund. Read his review: “Exposure to cutting-edge global businesses”

Local or Offshore?

Blog 43 – Local or Offshore? The debate on whether to invest locally or offshore has been raging again recently. Many financial commentators are comparing the returns on the JSE All Share index to the S&P 500 Index. The JSE All Share Index (ALSI) represents the broad South African stock market and the S&P 500 […]

Covid-19

Our Performance and Investment Strategy during the Covid-19 Pandemic.

Portfolio Manager’s Report as at 31 December 2019

LUNAR FR Worldwide Flexible Fund Investing is not easy because the market can behave in ways that is irrational in the eyes of investors or unexpected given investor sentiment and macro-economic trends. Our job as investors is thus to be able to sift through all the information that could affect share prices and identify those […]

Lunar BCI Worldwide Flexible Fund Three-Year Review

View PDF Three Years On July 10, 2019 On 1 June 2019, we celebrated three years since the launch of the Lunar FR Worldwide Flexible Fund. We are very pleased with the support that we have received from our clients, business partners and our management and staff. Our clients are in fact our co-investors. Founding […]

Who are you going to vote for?

Elections Everywhere Nigeria, Namibia, Indonesia, India, Spain, South Africa, …. Elections Everywhere. It seems like 2019 is the year of elections. As citizens, we are all interested and invested (in the broadest sense of the word) in the outcome of the election in South Africa, and maybe even in some other countries’ elections too. We […]

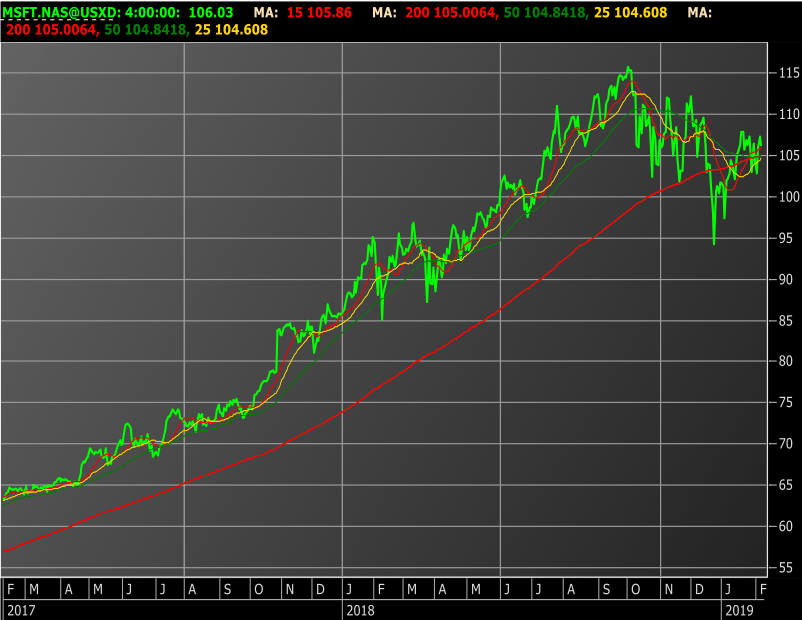

Share Focus: Microsoft (MSFT.NAS)

“Our strong commercial cloud results reflect our deep and growing partnerships with leading companies in every industry including retail, financial services, and healthcare,” said Satya Nadella, CEO of Microsoft. \”We are delivering differentiated value across the cloud and edge as we work to earn customer trust every day.” Microsoft’s mission is to empower every person […]

Time for a Rest

Listen to the podcast Transcript In a few days, many people will be taking some time off from work for their annual vacation. That is of course if they are fortunate enough to have a job. So, when I was thinking about this blog, several thoughts came to mind: Firstly, let’s do something different; […]

Good Markets, Bad Markets

Market Overview The market has been on a roller coaster ride over the last 3 months, showing good gains in August, but having a significant pull-back in September and October, both locally and offshore. The markets are largely driven by high valuations in the US; rising interest rates in the USA and Europe; and low […]

Active vs Passive

Market Overview A struggling local economy, flight of capital from emerging markets to developed markets, a volatile Rand and generally low or negative growth in company earnings have been the main drivers of the poor performance in the South African equity market. The Rand has weakened significantly against the major currencies (-12.8% YTD against the […]