What to do about the Rand?

[fusion_builder_container hundred_percent=\”no\” equal_height_columns=\”no\” menu_anchor=\”\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” class=\”\” id=\”\” background_color=\”\” background_image=\”\” background_position=\”center center\” background_repeat=\”no-repeat\” fade=\”no\” background_parallax=\”none\” parallax_speed=\”0.3\” video_mp4=\”\” video_webm=\”\” video_ogv=\”\” video_url=\”\” video_aspect_ratio=\”16:9\” video_loop=\”yes\” video_mute=\”yes\” overlay_color=\”\” video_preview_image=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” padding_top=\”\” padding_bottom=\”\” padding_left=\”\” padding_right=\”\”][fusion_builder_row][fusion_builder_column type=\”1_1\” layout=\”1_1\” background_position=\”left top\” background_color=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” border_position=\”all\” spacing=\”yes\” background_image=\”\” background_repeat=\”no-repeat\” padding=\”\” margin_top=\”0px\” margin_bottom=\”0px\” class=\”\” id=\”\” animation_type=\”\” animation_speed=\”0.3\” animation_direction=\”left\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” center_content=\”no\” last=\”no\” min_height=\”\” […]

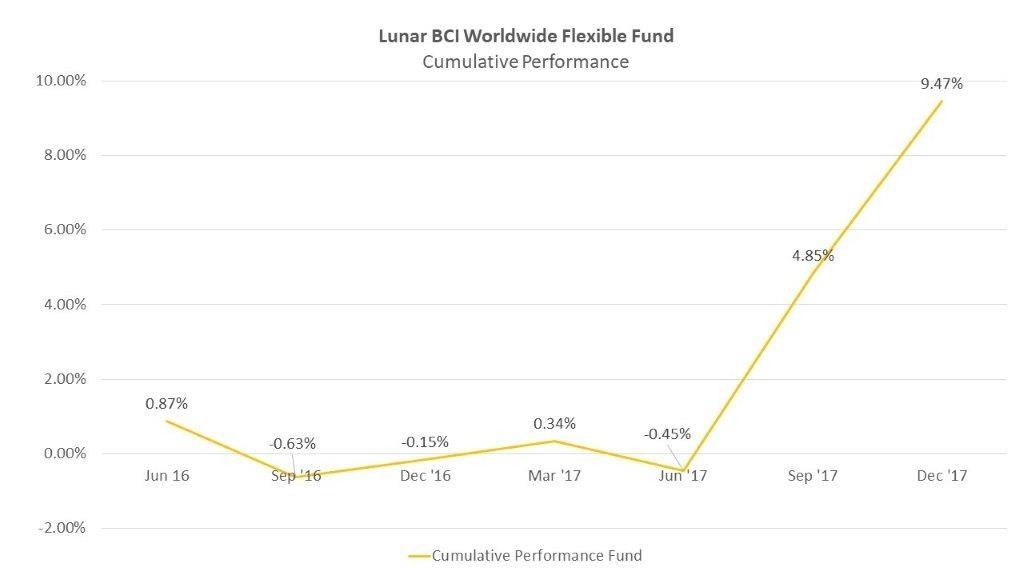

Lunar BCI Worldwide Flexible Fund Two-Year Review

[fusion_builder_container hundred_percent=\”no\” equal_height_columns=\”no\” menu_anchor=\”\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” class=\”\” id=\”\” background_color=\”\” background_image=\”\” background_position=\”center center\” background_repeat=\”no-repeat\” fade=\”no\” background_parallax=\”none\” parallax_speed=\”0.3\” video_mp4=\”\” video_webm=\”\” video_ogv=\”\” video_url=\”\” video_aspect_ratio=\”16:9\” video_loop=\”yes\” video_mute=\”yes\” overlay_color=\”\” video_preview_image=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” padding_top=\”\” padding_bottom=\”\” padding_left=\”\” padding_right=\”\”][fusion_builder_row][fusion_builder_column type=\”1_1\” layout=\”1_1\” background_position=\”left top\” background_color=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” border_position=\”all\” spacing=\”yes\” background_image=\”\” background_repeat=\”no-repeat\” padding=\”\” margin_top=\”0px\” margin_bottom=\”0px\” class=\”\” id=\”\” animation_type=\”\” animation_speed=\”0.3\” animation_direction=\”left\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” center_content=\”no\” last=\”no\” min_height=\”\” […]

Hubris

Hubris Investors are faced with a multitude of risks in any investment decision that they take. With the recent results from Famous Brands, Mediclinic, Taste Holdings and also not so recently Woolies and Old Mutual; one can’t help wondering if executive hubris* is not one of the bigger risks that investors face. Offshore Expansion […]

The Land Question?

In my opinion, the Land Question in South Africa raises a broader issue. It is the question of retribution for the crimes of colonialism and Apartheid. The Black Economic Empowerment policies attempted to address these issues but these have fallen short of meaningful empowerment of the previously disenfranchised. It has also had unintended consequences – […]

Goals Conceded, Saved, Missed and Scored

[fusion_builder_container hundred_percent=\”no\” equal_height_columns=\”no\” menu_anchor=\”\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” class=\”\” id=\”\” background_color=\”\” background_image=\”\” background_position=\”center center\” background_repeat=\”no-repeat\” fade=\”no\” background_parallax=\”none\” parallax_speed=\”0.3\” video_mp4=\”\” video_webm=\”\” video_ogv=\”\” video_url=\”\” video_aspect_ratio=\”16:9\” video_loop=\”yes\” video_mute=\”yes\” overlay_color=\”\” video_preview_image=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” padding_top=\”\” padding_bottom=\”\” padding_left=\”\” padding_right=\”\”][fusion_builder_row][fusion_builder_column type=\”1_1\” layout=\”1_1\” background_position=\”left top\” background_color=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” border_position=\”all\” spacing=\”yes\” background_image=\”\” background_repeat=\”no-repeat\” padding=\”\” margin_top=\”0px\” margin_bottom=\”0px\” class=\”\” id=\”\” animation_type=\”\” animation_speed=\”0.3\” animation_direction=\”left\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” center_content=\”no\” last=\”no\” min_height=\”\” […]

Lunar BCI Worldwide Flexible Fund End of Year 2017 Report

Market Overview The calendar year 2017 was another roller-coaster year for the investment markets in South Africa and globally. Some of the more significant events include: Ratings agencies downgraded South African sovereign debt to junk status, citing political and economic risks facing the country; Serious allegations of mismanagement and corruption in state-owned enterprises, including Eskom, […]

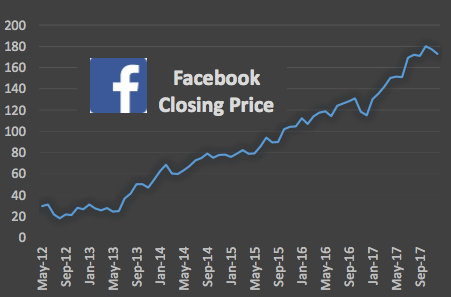

Share Focus: Facebook

[fusion_builder_container hundred_percent=\”no\” equal_height_columns=\”no\” menu_anchor=\”\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” class=\”\” id=\”\” background_color=\”\” background_image=\”\” background_position=\”center center\” background_repeat=\”no-repeat\” fade=\”no\” background_parallax=\”none\” parallax_speed=\”0.3\” video_mp4=\”\” video_webm=\”\” video_ogv=\”\” video_url=\”\” video_aspect_ratio=\”16:9\” video_loop=\”yes\” video_mute=\”yes\” overlay_color=\”\” video_preview_image=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” padding_top=\”\” padding_bottom=\”\” padding_left=\”\” padding_right=\”\”][fusion_builder_row][fusion_builder_column type=\”1_1\” layout=\”1_1\” background_position=\”left top\” background_color=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” border_position=\”all\” spacing=\”yes\” background_image=\”\” background_repeat=\”no-repeat\” padding=\”\” margin_top=\”0px\” margin_bottom=\”0px\” class=\”\” id=\”\” animation_type=\”\” animation_speed=\”0.3\” animation_direction=\”left\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” center_content=\”no\” last=\”no\” min_height=\”\” […]

Delaying Gratification

[fusion_builder_container hundred_percent=\”no\” equal_height_columns=\”no\” menu_anchor=\”\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” class=\”\” id=\”\” background_color=\”\” background_image=\”\” background_position=\”center center\” background_repeat=\”no-repeat\” fade=\”no\” background_parallax=\”none\” parallax_speed=\”0.3\” video_mp4=\”\” video_webm=\”\” video_ogv=\”\” video_url=\”\” video_aspect_ratio=\”16:9\” video_loop=\”yes\” video_mute=\”yes\” overlay_color=\”\” video_preview_image=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” padding_top=\”\” padding_bottom=\”\” padding_left=\”\” padding_right=\”\”][fusion_builder_row][fusion_builder_column type=\”1_1\” layout=\”1_1\” background_position=\”left top\” background_color=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” border_position=\”all\” spacing=\”yes\” background_image=\”\” background_repeat=\”no-repeat\” padding=\”\” margin_top=\”0px\” margin_bottom=\”0px\” class=\”\” id=\”\” animation_type=\”\” animation_speed=\”0.3\” animation_direction=\”left\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” center_content=\”no\” last=\”no\” min_height=\”\” […]

Thinking about my biggest investing mistakes

Shhh.. As the Naspers (NPN) share price keeps on powering ahead, I can’t help thinking why did I ever sell the Naspers I bought for my wife’s portfolio a few years back (Shhh.. please don’t tell her). In 2010, I bought some Naspers for my wife’s account for around R298 per share. Within a period […]

Interview with Sabir Munshi on what is Bitcoin and what the future may hold for Bitcoin

[fusion_builder_container hundred_percent=\”no\” equal_height_columns=\”no\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” background_position=\”center center\” background_repeat=\”no-repeat\” fade=\”no\” background_parallax=\”none\” parallax_speed=\”0.3\” video_aspect_ratio=\”16:9\” video_loop=\”yes\” video_mute=\”yes\” overlay_opacity=\”0.5\” border_style=\”solid\”][fusion_builder_row][fusion_builder_column type=\”1_1\” layout=\”1_1\” background_position=\”left top\” background_color=\”\” border_size=\”\” border_color=\”\” border_style=\”solid\” border_position=\”all\” spacing=\”yes\” background_image=\”\” background_repeat=\”no-repeat\” padding=\”\” margin_top=\”0px\” margin_bottom=\”0px\” class=\”\” id=\”\” animation_type=\”\” animation_speed=\”0.3\” animation_direction=\”left\” hide_on_mobile=\”small-visibility,medium-visibility,large-visibility\” center_content=\”no\” last=\”no\” min_height=\”\” hover_type=\”none\” link=\”\”][fusion_text] Sabir Munshi Director at Lunar Capital talks Salaamedias listeners through a number of questions […]